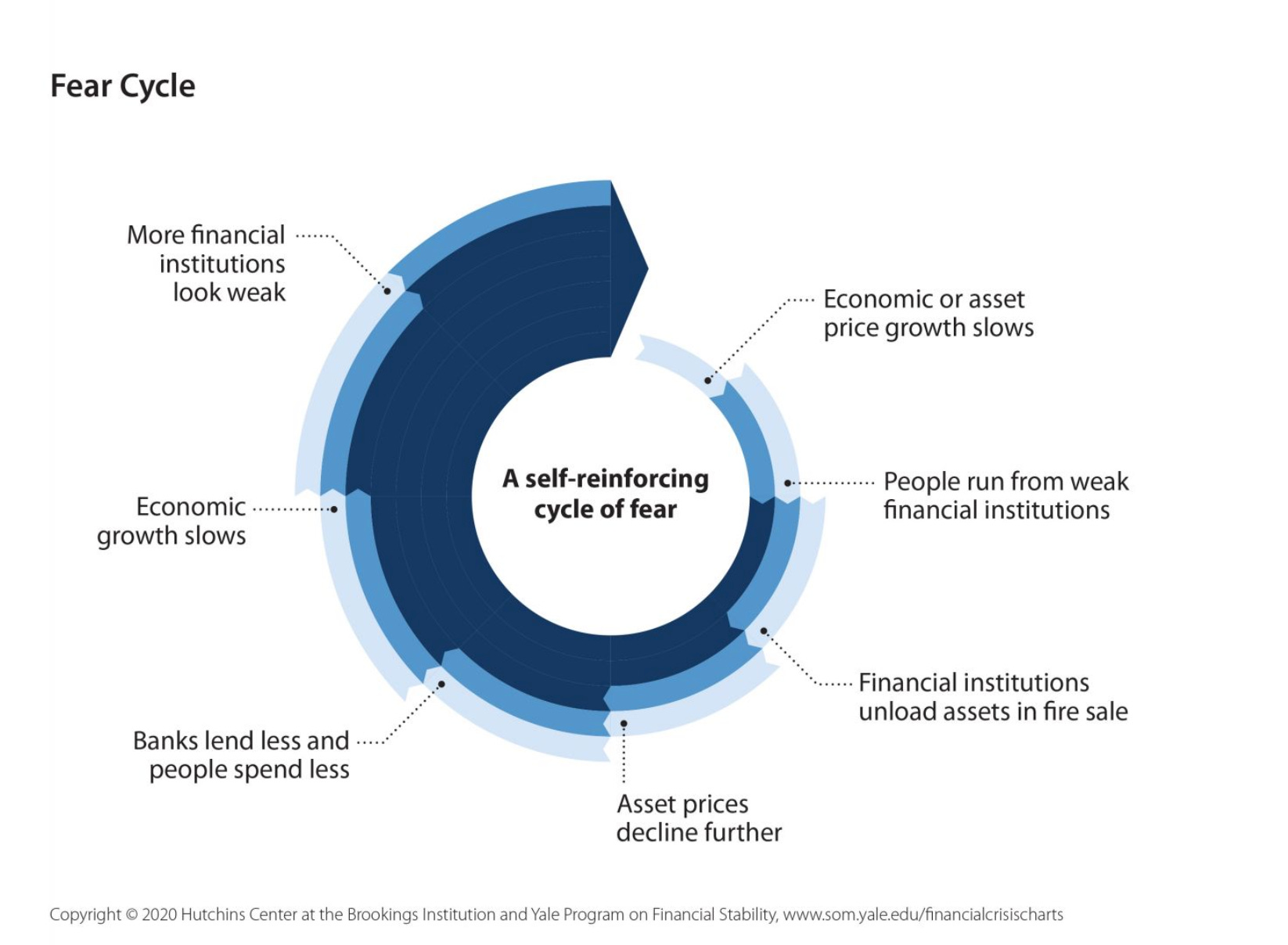

How about a series of mini-GFCs?

Watch the acronyms--they're going to be important

Outstanding household debts in the form of mortgages amount to a $12 trillion (approx.) market in the US. Roughly half of the total credit risk related to that market—the risk that homeowners will default—is now held by private investors in the form of CRT (Credit Risk Transfer) bonds issued by Fannie Mae and Freddie Mac (the GSEs). Some substantial portion of those bonds is actually riskier than standard metrics show, because longterm climate risk in specific locations isn't adequately being taken into account--at least, that's the argument David Burt of DeltaTerra Capital is making. (I wrote about Burt last week here.)

Burt is using high-resolution climate data and other tools to predict that property values in "exposed" risky markets—something like 20 percent of all US houses—will fall by between $1.2 and $1.9 trillion, causing a cascade of defaults. He says this will be like a bunch of mini-Great Financial Crises (GFCs) happening in the 20 percent of communities exposed to location-based risks of "ownership challenges" and rapidly increasing insurance premiums that are already hitting homeowners. This should be alarming: Even 20 percent of a 2008-style sell-off is something no one wants to live through.

It turns out that CRT bonds have similarities to catastrophe bonds: they're bets that awful, extreme things won't happen to homeowners in the US. Like cat bonds, the risks associated with CRTs are substantially higher than Treasuries, but returns can also potentially be higher. No doubt the institutional investors, risk-tolerant high-net-worth individuals, and investment funds who buy CRTs know all about this. But in the context of rapidly-accelerating climate change, the "ordinary" volatility of creditworthiness and asset values for a substantial chunk of the $45 trillion single-family property market will be amplified in ways that even those investors may not be anticipating.

Burt's overall assessment is that if climate change continues along the "business as usual" path (which seems to be happening), about half the $52 billion in outstanding CRT bonds will experience a loss of 20% or more. He's predicting that about half the $11 billion in junior or subordinate tranches of residential mortgage-backed securities issued by private entities, not the GSEs, will experience similar losses, and about 20 percent of subordinate commercial mortgage-backed securities will go down by between 5 and 20 percent.

Along the way, some loans will do really well and some will do very badly. This will be difficult for the flow of credit; Burt is implying that in a couple of years the credit markets will tighten up sharply as everyone suddenly wakes up to the risks and systemic repricing (or, really, rethinking!) of properties happens.

Each CRT bond is connected to between 50,000 and 180,000 loans from different parts of the country that, for example, all have a similar loan-to-home-value ratio. (That's why, absent fine-grained climate data, you wouldn't necessarily know what climate risks were lurking in an individual bond.) These bonds are at once simpler and more complicated than you might think. Here's a useful diagram:*

GSEs, in the middle, buy mortgages from banks by essentially using money raised from investors in mortgage-backed securities (MBS)—that's the "mortgage pool"—in what amounts to a pass-through. The payments made by homeowners go right to the MBS investors. "Buying" mortgages this way allows the GSEs to shift to those investors the risk of interest rates going up or down (prompting refinancings and prepayments) over the 30-year life of a mortgage. In exchange for access to this capital, the GSEs are paid a "guarantee fee" (the "G-fee" in the diagram) that is added to the homeowner's monthly payment.

The MBS investors are willing to take on interest rate risks, but they don't want to have to worry about whether borrowers will default. So the GSEs shift credit risk to a different set of investors: institutions and individuals who buy Credit Risk Transfer bonds.

Like cat bonds, these work by creation of a pool of money from investors (the "CRT Capital" in the diagram, which is a trust) that is left untouched unless some trigger of percentages of defaulting loans is met. In exchange for leaving their money in this pool, the CRT investors are regularly paid—the "Coupon payments" in the diagram—a portion of the G-fee. This is a risky endeavor for the CRT investors, so the fee paid to them will be in the range of what below-investment-grade (junk) corporate bonds pay. But the fee doesn't vary by location of the underlying properties.

When the trigger is reached—say, 7.5 percent of loans in a given bond pool go into default—the GSEs can begin being reimbursed for those losses by drawing down on the CRT Capital. When things get really catastrophic, and defaults reach a really high level (another trigger set up in advance), the GSE steps back in and absorbs further losses.

If defaults never reach that first figure, the CRT investor does well: they get those high regular payments and the principal left in the CRT Capital pool is returned to them untouched when the bonds mature. If losses have been very high, the investors may get nothing at maturity. Burt's thesis is that rising insurance costs and climate risks in about a fifth of the US housing market will lead to declining property values and thus higher risks of default (and/or properties that aren't valuable enough to cover the loan amounts when a default occurs), making CRT risks higher in some instances than investors may believe.

The CRT structure was set up to shift the first losses on these credit risks to the private sector. It's been successful on that front: since 2013, credit risk associated with more than $6.2 trillion in unpaid principal balances on loans held by the GSEs has been transferred in this fashion.

Now, the GSEs—the public—will take back risks after that second trigger kicks in. Which parts of this ecosystem have enough accurate, sufficiently climate-informed data to help them make decisions? Homeowners? Lenders? the GSEs? CRT investors? What can be done to forestall a hard systemic repricing that harms homeowners?

Time will tell.

Here's the action step: the Federal Housing Finance Agency has issued a call for papers for an "Econ Summit on Climate-Related Risks to Housing" later this year. They're looking, among other topics, for information about "loan performance in the wake of natural disasters." Go forth, keeping in mind the threat of another GFC—the cataclysm of 2008 that's now, apparently, an acronym.

*From "The Market View of Mortgage Credit Risk," a 2022 PhD thesis by James O'Neill available here.