It's still easy to buy a home in a climate risky area. It's harder to sell it.

Fintech lenders are more likely to approve loans in high climate risk areas, but property values in those areas are dropping.

Two studies out this week signal the short-term/long-term problem of coastal housing in our era: It will likely continue to be relatively easy to buy a new home in a climate-risky area—just get a mortgage from a nonbank lender—but people will soon discover that it is much harder to sell. One of these studies shows that non-traditional online lenders are more likely to approve loans in high-risk areas, the other that high-risk properties along the Atlantic and Gulf Coast will be losing value.

The liquidity crunch is beginning. Meanwhile, this week's talk about privatizing Fannie Mae and Freddie Mac—while retaining some kind of "implied guarantee" that the federal government will step in if they go under—suggests that climate-risky loans will continue to be effectively subsidized by these entities. It's a one-way ratchet of risk, all slowly playing out as hurricane season begins.

Tyler Haupert and Jesse Keenan's newly-posted report, "Bluelining in Red Hot Fire Zones: Fintech and Traditional Mortgage Lending in California's Wildfire Risk Zones," separates mortgage lenders into two groups: those that issue mortgages online, without a phone call or meeting—"fintech" lenders like Rocket Mortgage and PennyMac—and more traditional banks, like Citibank. The authors combined detailed information about mortgage applications in California, drawn from public Home Mortgage Disclosure Act data for 2018-2020, with natural disaster risk scores from FEMA's National Risk Index. It turns out that traditional lenders see mortgage applications for a home in a neighborhood with high wildfire risk as much riskier than online fintech lenders do. This may be because fintech lenders don't operate locally and don't have the same soft information about physical climate risk that the traditional lenders have. We might have guessed as much. They're operating in an automatic way.

But the authors also find that fintech lenders are more likely to approve loans in high climate risk neighborhoods than in neighborhoods with little or no physical risk from climate change. That's surprising. It signals that these nonbanks, which are rapidly consolidating, are so good at immediately selling off—securitizing—loans to other investors, shifting the risk away from themselves, that it's worth it for them to keep mortgages flowing in risky areas, generating fees.* This means that there aren't price signals coming from fintech lenders in the form of higher interest rates that might moderate house-buying behavior in climate-threatened places. It also suggests that the continued appetite for houses in these places will make it difficult for land-use planners to nudge people to live elsewhere.

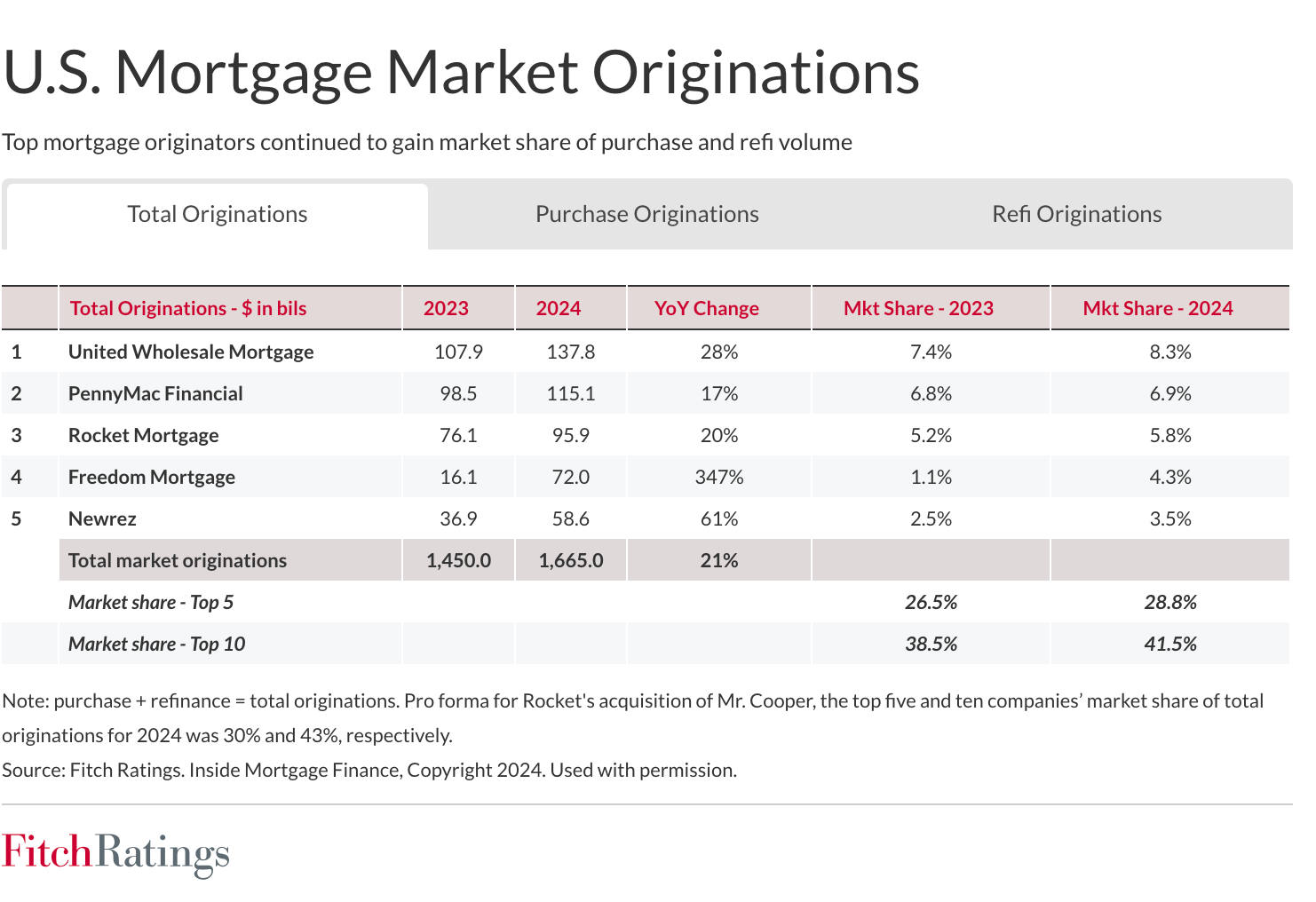

The top five fintech, non-bank lenders originated about 30 percent of mortgages in the US in 2024, according to Fitch Ratings, and as of 2022 were managing most of the country's mortgages.

I don't know exactly how many of the loans fintech firms originate are bought and securitized by Fannie Mae and Freddie Mac, but I do know it's very substantial; nonbanks account for most of the mortgages handed over to the GSEs.

This study looked at wildfire in California, but the incentives that motivate fintech behavior—driven by algorithm, a business model that relies on passing risks to Fannie Mae and Freddie Mac, a desire for market share in areas a traditional bank might avoid—are highly likely to operate along the Atlantic and the Gulf Coasts as well, well hurricanes and floods are a growing risk.

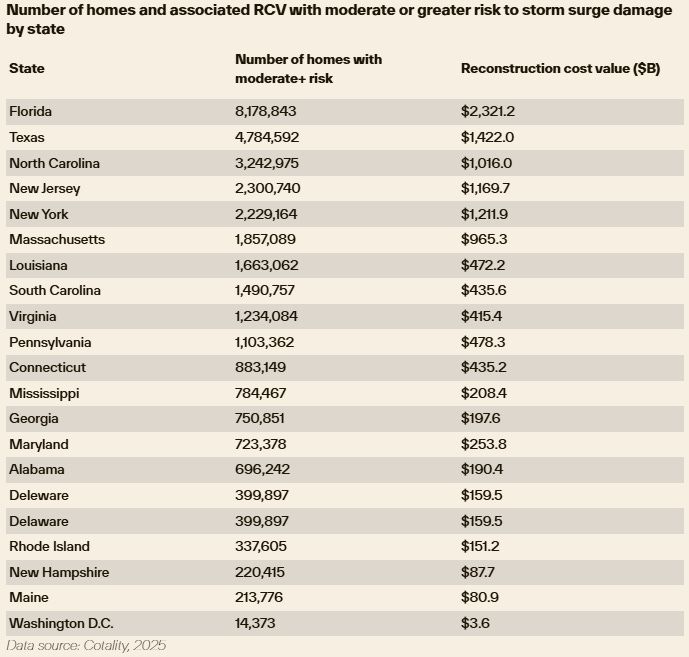

Houses near the Atlantic and the Gulf are facing sharp devaluations, sooner than most people think. The firm formerly known as CoreLogic, now renamed Cotality (not a beautiful name, but certainly distinctive) put out a 2025 Hurricane Risk report at the end of last week estimating that 6.4 million coastal homes in Atlantic and Gulf Coast states, with a replacement cost of $2.2 trillion, were at very substantial risk from storm surge. That's a subset of these 35.3 million homes (and $10.1 trillion in value) that are at "moderate or greater risk") for storm surge:

In its report, Cotality deploys a useful term for what is happening visibly in some Florida areas, and inevitably in others: as the risk of flood damage grows, insurance becomes less available and less affordable, properties lose value and sit on the market longer, and owners find themselves in a "liquidity trap."

All of this adds up to increasing risk that will be borne by homeowners and taxpayers, directly or indirectly. It's quite a flywheel: The increasingly consolidating growth machine of non-banks is churning out ever more loans while ignoring physical climate risks.

Those loans keep going only because states and localized insurers are providing increasingly risky and expensive insurance to back them. As Fitch Ratings recently noted in Florida, Citizens (the state's insurer of last resort) is moving to "depopulate" its public rolls by forcing people onto private insurance. But the local Florida insurers willing to write policies may not be able to withstand the challenges they will face: "Florida specialty insurers’ capital tends to be weaker than larger, national peers and could be challenged by a significant catastrophe year." It's highly likely that this situation prevails in most of the other Atlantic and Gulf Coast states where national insurers are backing away from flood-prone properties. As on-the-edge homeowners experience more flooding, find their underinsured risks to be great, and can't afford yearly premiums, they will default or sell at a loss, pre-paying their mortgages and moving on.

Meanwhile, future climate awareness within Fannie Mae is actively discouraged by the current administration, which dreams of privatization. But, one way or another, privatization will likely cause a jolt to coastal homeowners and the rest of us: Won't private investors insist on accurately-priced risk, sharply raising the cost of mortgages? And if some form of "implicit guarantee" is kept in place, doesn't that keep taxpayers on the hook for the built-in consequences of physical climate risks that have been (effectively) deliberately subsidized by Fannie Mae's underpricing policies?

We are making our $13 trillion housing finance system more vulnerable to the physical impacts of climate change with each passing month. It's going to be quite a summer.

Image of Hurricane Milton from NOAA's GOES-16 satellite on Oct. 8, 2024. (Image credit: NOAA)

* Nonbanks don't hold deposits, and so they're basically unregulated at the federal level. They are mostly overseen by states and by the Consumer Financial Products Bureau, but their duties are light. Nonbank mortgage loans are usually sold to Fannie Mae or Freddie Mac in large bundles that are then securitized as mortgage-backed securities, but the originating nonbank often retains the contract to "manage" or "service" the loan by collecting payments.