Make Housing Affordable Again—but not in a flood zone

DC's deregulation plans ignore the physical risks of climate change

Newport RI flood map, from the Rhode Island Floodplain Viewer. White area is current 500-year (.2 percent annual risk) flood zone; light blue is 100-year (1 percent annual risk) flood risk area; darker blue is combined storm surge and flooding 1 percent annual risk. Map does not incorporate projected risk due to accelerating climate change.

Housing was a key issue in the 2024 election. We're short between 4 and 7 million homes, and Americans believe affordable housing is a particularly thorny problem. The Trump administration is taking advantage of this crisis to push for deregulation of building standards—particularly those that relate to flood and other climate-related risks.

Both developers and lenders want federal regulators to loosen whatever rules they can. Their pitch—that lowering standards will provide opportunities to build and finance more housing—meets the moment. Federal regulators now in office will be happy to oblige, even if that means encouraging building in areas that insurance companies are already exiting because of concerns about exposure to losses driven by the physical effects of climate change.

From The New York Times. Two insurers have stopped writing new policies in Rhode Island, one has gone into receivership, and many more homeowners have been pushed into the state’s insurer of last resort, paying premiums that are 40-50% higher for narrower coverage.

After these homes are built, the developers, having made their money, will move on to other projects. Mortgage originators, meanwhile, collect their fees and shift the risks to Fannie Mae and Freddie Mac—entities that were already slow to account for physical climate risk before the new administration came to town and now will likely stop altogether.

As the administration looks to "Make Housing Affordable Again," Americans should be asking: Is a house that is chronically flooding truly affordable, either for the person who buys it or for the country as a whole? We're heading into another unusually busy hurricane season for the Atlantic. But storms aren't the only threat: Scientists are saying that the rate of high-tide flooding could accelerate along the East Coast much sooner than anyone thought even ten years ago.

FHFA Director William Pulte and Mortgage Bankers Association Chair Laura Escobar, May 19, 2025. Asked about ways the FHFA could boost housing supply to make housing more affordable, Pulte said the federal government’s role would be largely focused on deregulation.

This past month, Federal Housing Finance Agency (FHFA) Director William Pulte spoke to the Mortgage Bankers Association (MBA) and, at length, to Donald J. Trump Jr. on his podcast, "Triggered." Director Pulte, who leads the agency that regulates Fannie Mae and Freddie Mac, chairs both their boards, and dismissed more than a dozen board members from both companies, has a clear deregulatory direction. "We need municipalities who are going to work with us to get more units built and get people back in homes in this country," he told Don Jr.

That work has included getting the government to stop requiring that affordable housing using HUD funds or FHA mortgage insurance comply with federal flood risk standards that require increased elevation or floodproofing in more broadly-defined floodplains (going beyond the increasingly inadequate 1-percent-annual-risk-of-flooding areas in which federal flood insurance is needed to get a mortgage).

From the mortgage originators' perspective, the floodplain rule's science-based approach and elevation requirements "threaten affordable housing production by introducing unclear, burdensome challenges"—and the MBA is asking that the rule be repealed entirely. This means that affordable housing won't meet modern, forward-looking standards. In the long run, both renters and homeowners will be stuck in damp, unlivable, and dangerous swamps.

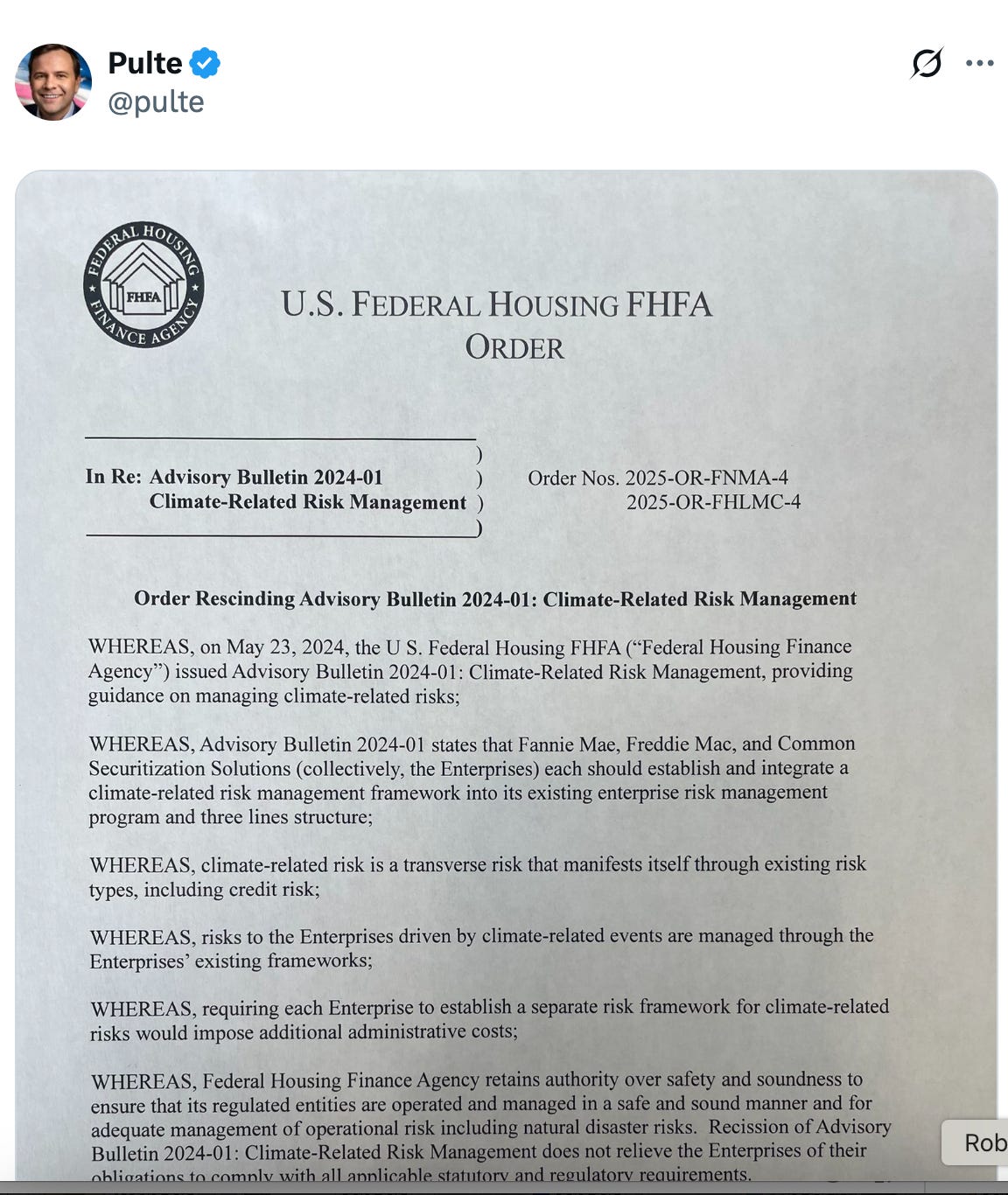

Two months ago, Director Pulte, by tweet, revoked the guidance FHFA had put together last year urging Fannie Mae and Freddie Mac to take physical climate risk into account:

Pulte has a long history of being a builder: His grandfather, also named William Pulte, built Pulte Homes into the largest home builder in America. He will want to incentivize new construction, no matter what—and lowering physical climate risk, for him, likely falls into a politically contentious and wholly unnecessary category of DEI and climate issues that are now off the table. Pulte's FHFA will not be looking to push disclosures of flood risk, or to price those risks into mortgages—indeed, they'll actively avoid doing so. Meanwhile, insurance companies—the most liquid part of this entire housing finance system—are rapidly exiting riskier areas and charging more for less, and defaults/foreclosures are following on the heels of flood events.

(At the same time, Director Pulte is working with the administration to figure out how to privatize Fannie Mae and Freddie Mac—a transaction that would be effectively the largest IPO in history, requiring trillions in new cash. What could go wrong? I'll say more about this next week.)

Meanwhile, back in reality, a new study out this month in Nature warns that our current rate of accelerating heating has likely already destabilized polar ice sheets, which are already contributing four times as much to global sea level rise compared to thirty years ago. We may be seeing a foot a year of sea level rise in a matter of decades, with even more water sloshing up on the East Coast.

This is a key bit: "Palaeo-records and numerical modeling also demonstrate that ice sheets exhibit highly non-linear responses to climate forcing and are sensitive to temperature thresholds that, once crossed, lead to rates of SLR much higher than present." We know from the past that ice sheets can melt at an explosive, ferocious rate, much faster than what we're already seeing today (which is already much faster than it used to be). Feet per decade. This would be catastrophic for coastal communities everywhere, and particularly here.

So, yes, let's Make Housing Affordable Again. But let's not make it dangerously risky. Listen to the insurance companies. They have data that banks, apparently, don't.