Safe as houses: How muni credit-rating agencies help keep the status quo in place

Even though physical climate risks are accelerating, you wouldn't know it from the market for long-term municipal bonds

There are high-net worth investors in America who bought 30-year general obligation muni bonds coming out of Florida this week. They wanted the regular, fixed, federal-tax-free income that these bonds will generate every six months. They wanted long-duration, relatively-high-interest assets on hand as interest rates in other places where they might park cash keep going down. They were diversifying their investment portfolios.

Imagine these guys buying bonds while the news of Hurricane Helene's ferocity is playing on their office televisions. The sound is muted, so the terrified, wind-whipped reporter holding his slicker out of his eyes while he yells into his microphone can't be heard.

Let's say the investor is quite sophisticated about physical climate risks. He may know that Blackstone is quietly unloading houses it owns in Florida because rising costs of property insurance are making it uneconomic to continue owning them.

He may even work for an insurance company—a sector that soaks up lots of muni bonds—and know that the real estate market in Florida likely will not be recognizable in 30 years. But he is absolutely driven by the possibility of tax-free yield.

He has no incentive to notice that credit rating agencies looking at a city in Florida, or a city in Arizona, simply assign the city a rating—and don't change that rating when they're looking at a bond that is supposed to return its principal to the bondholders 30 years from now. That 30-year maturity bond gets the same rating that a 4-year bond issued by the same city gets.

There's an entire muni bond machine, fueled by credit ratings, that is pumping away right now without looking at how the physical world will change over the next thirty years. That's bananas.

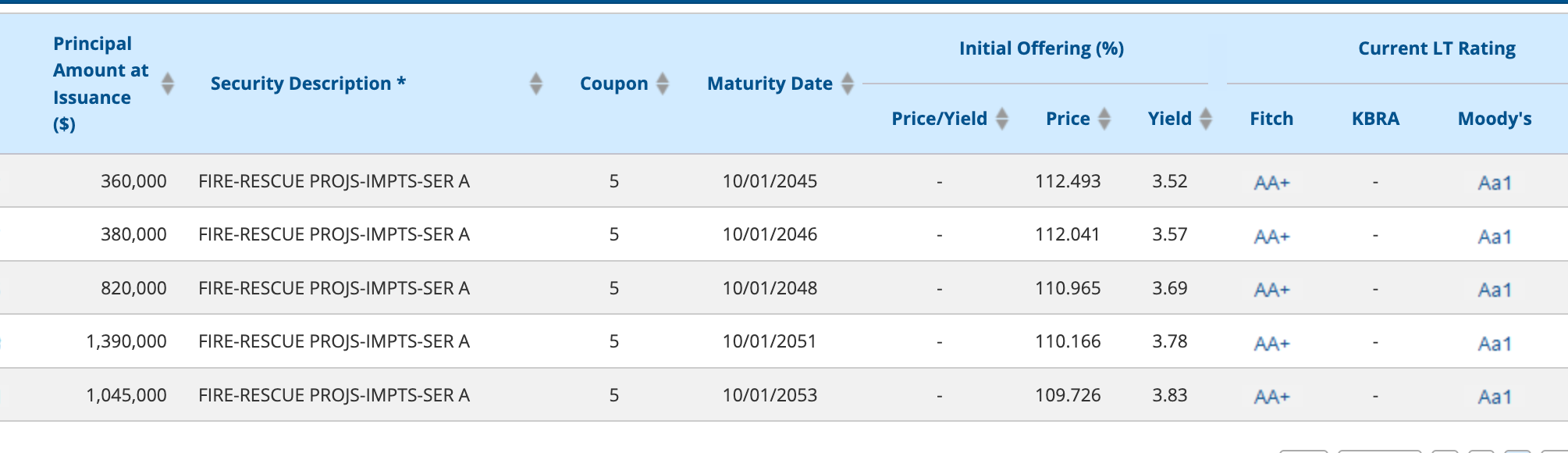

Here's an example. Take Pasco County in Florida. It's on the coast. Hurricane Helene caused catastrophic 16-feet storm surge in Pasco County yesterday, and 135 people had to be plucked out of the water. Well, earlier this year Pasco County issued a "general obligation" bond backed by the full faith and credit of the county—and thus its future property tax revenues. The credit rating assigned by Fitch and Moody's to the 10-year chunk of this bond, maturing in 2035, is the same as the rating for the chunk that won't mature for another 29 years.

Ratings for bond issued by Pasco County that will mature in 2053 are the same as ratings for 2035.

And Fitch upgraded Pasco County just before the bond went out to the market, to "AA-plus," the second-highest rating it gives. Bonds lasting 29 years issued by a climate-threatened coastal county where many people are living no more than five feet above sea level are being labeled as low risk.

In fact, not only are credit ratings for climate-threatened cities issuing bonds uniform over decades—years in which we know these cities' physical conditions will be shifting—but they're also very high: credit rating upgrades are outpacing downgrades. Miami, the bubbliest of the bubbles, was upgraded to AA from AA-minus last year by Fitch. Phoenix, facing dwindling Colorado water levels, this summer got the second-highest rating, Aa1, that Moody's gives out.

What's going on?

Some of these higher ratings are likely based on short-term infusions of COVID funding that are still working their way through city budgets. But the larger answer seems to be that the rating agencies are looking only at short-term fiscal capacity while facilitating the sale of long-term obligations that will inevitably be affected by physical climate change.

Pasco, Miami, and Phoenix will probably be able to cover their debts next year, in other words. That's what's relevant to the rating agencies. In 30 years, after some property owners who can't get insurance and can't sell their houses—and have had enough—leave, will the property tax revenue still be there in case it's needed to pay back what's owing? What property taxes will be paid if Phoenix can't get access to water? (Phoenix issued a $500 million general obligation bond program last November.) If Pasco County melts into the sea? Hard to say.

But the future is not the focus for the rating agencies, the investors, or the cities themselves. All three have a keen interest in keeping the machine spinning. The rating agencies are paid by issuers to produce their ratings. The investors like to shield income from taxes. And people managing cities need all the capital they can get, and they're going to grab it while they can—issuance this year is way up over 2023.

Stephanie Larosiliere, Invesco's head of fixed income, business strategy and development, discusses how the Federal Reserve's rate cut impacts the municipal bond market. She spoke on the Sept. 19 episode of "Bloomberg The Close."

There's a larger theme here: the lack of place-based, time-aware credit rating will push risk onto the shoulders of the federal government—all of us. When a city can't cover its debts, it will go into bankruptcy. There will be a frantic call for federal assistance. And then we'll all be in the soup.

In the meantime, watch the muni machine carefully. It's masking a mountain of risk at an incredible clip: $40 billion in municipal bonds will be issued this month alone and the long-term bonds are selling particularly well. Watch AAA-rated bonds suddenly become worthless when cities and counties can't keep up.

I bet there are investors who are betting right now that the prices of these bonds will go down. When the machine is running well, there are many people who are content to push things along. When it breaks down, we will see who actually understood why it was working at all.

I assume there's a way to short these bonds?

I’m sure you’re right. Smart people out there will make a lot of money in this market.