Why pushing to rebuild quickly in LA is both understandable and unthinkable

Short term thinking even as a loud warning about the effects of accelerating climate change on global financial wellbeing rings out

Rapidly accelerating climate change likely contributed to the ferocity of the fires in Los Angeles this past week, with huge and growing swings between wet and dry years supercharging both the availability of fuel—two wet years prompting plant growth—and its desiccated state this January following months of hot and dry weather. Fire isn't a new problem for the area: humans have been experiencing Santa Ana winds sweeping through the canyons toward the sea and hillsides exploding with flames for hundreds of years.

But the increasing risk of devastation by fire in Los Angeles is amped up by dramatic development in fire-prone areas. It's not just happening in LA: According to Ben Christopher of CalMatters, nearly 45 percent of the homes built in California over the last 30 years have been in wildland-urban interface (WUI) areas. These are very risky places to live. They are the places where the vast majority of California structures destroyed by wildfires over the last forty years used to stand. Just as "it only floods where it floods," houses only burn down where they are built.

In the face of these increased risks, what’s the right role for government? Well, according to Gov. Gavin Newsom, the right role for the public sector is to get things back to the way they were before the Palisades Fire began to wreak havoc in Los Angeles. As quickly as possible.

Over the next few years, Los Angeles will host the World Cup, the Super Bowl, and the Olympics. From Gov. Newsom’s perspective, these events "reinforce the imperative [of] moving quickly" to rebuild. "This is an opportunity," Gov. Newsom says, for California and its destroyed communities "to shine," to feel the "pride and spirit that comes from not just hosting those three iconic games and venues, but also the opportunity I think to rebuild at the same time."

Newsom is organizing a "Marshall Plan to help Los Angeles rebuild faster and stronger." He's suspending permitting holdups and environmental reviews that might slow rebuilding (even though a California appellate court held late last year that increased wildfire risk, and lack of wildfire evacuation routes, are consequences of development that may deserve just this kind of review).

That's arguably the right short-term political response. Gov. Newsom wants to keep his job by showing urgency and resolve in the face of fires that have claimed more than two dozen lives and burned more than 40,000 acres. And it feels both glib and heartless to suggest that state and local officials pause before launching into unrestrained talk about rebuilding. After all, rebuilding in the same place, and often in exactly the same way, is what usually happens after cataclysmic California fires.

This time, though, is different. This is a moment when long term, thoughtful leadership is desperately needed. As BlackRock CEO Larry Fink says, rebuilding will be a long process. The parameters for that rebuilding need to be set now, and they need to be transformative.

There is a need for severe restrictions on building in risky areas, including increased building code and road design standards—at the least, the state needs to ensure that local authorities in all areas are enforcing what California's 2008 standards require for fire-risky areas.* These requirements need to be applied to existing, pre-2008 houses, not just new construction. Embers spread from house to house, so entire communities need to be safer, not just individual homes. The priority should be to support dense housing in safer areas, not single family homes in risky sections.

Without hard, sustained work on these standards and priorities, and on limiting building in the riskiest spots, it is far less likely that a truly functioning insurance market will ever re-emerge in California. At the moment, there is a significant potential that the FAIR Plan's insolvency will push assessments right into the pocketbooks of California policyholders, as I wrote last week. Some areas will likely become uninsurable and thus even more precarious for home owners. California needs more housing, and more dense housing, but it doesn't need more risky housing.

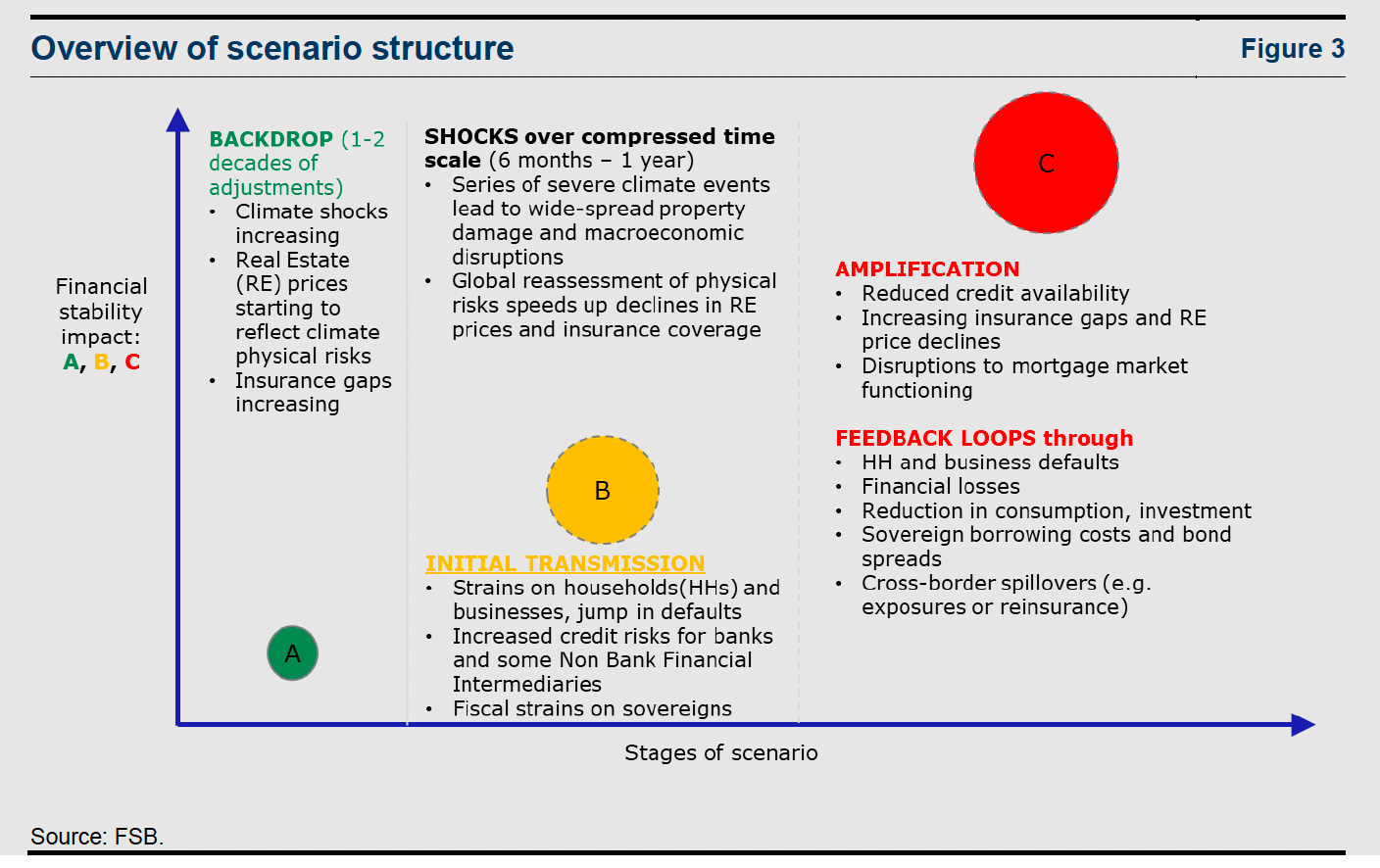

Even before these cataclysmic fires, keeping the status quo in place in Los Angeles (and other risky areas around the US) has built up systemic financial risk that may affect our overall economy. Today's Financial Stability Board report (FT story here) points out that rising insurance premiums and insurer exits (already clear in California) are leading indicators of unstable housing markets that, when hit by extreme weather events, may weaken banks, lead to freezes on lending, cause abrupt repricing of physical assets, and create fiscal strains on national economies by driving up both borrowing costs and direct expenses. In California, the narrative moved this week from A to B in the FSB's climate-risk scenario planning:

After the world saw how quickly financial vulnerabilities spread around the globe, triggering the 2007-08 financial crisis, the Financial Stability Board was created to watch for those signals. Now the FSB is saying that international financial stability requires putting accelerating physical climate change risks on the table, taking them into account, and planning ahead. Not racing to keep things just as they are so that the Olympics can come to town. Remember 2008, the FSB is saying, and then consider that physical climate risk is permanent and accelerating.

When it comes to technology innovation, air quality remediation, and a host of other policy domains, California has routinely led the nation. Here's another chance.

*Currently, application of the 2008 standards in areas where a local authority provides its own fire-fighting services (as opposed to unincorporated areas served by CAL FIRE) depends on whether the local authority has accepted designation as a Very High Fire Hazard Severity Zone.

We need a whole of industry response which the FSB has identified is part of the problem. Insurers who don’t pay out 100% if homeowners don’t rebuild exactly as before are a big part of the problem, just as they were in 2008 with credit default swap insurance. Identifying this as a huge risk to financial markets is a gift. Reminds me of the Great Salad Oil Swindle of 1963 - looks great on top until you peel back the onion.